PART 2 - TONI BRAXTON

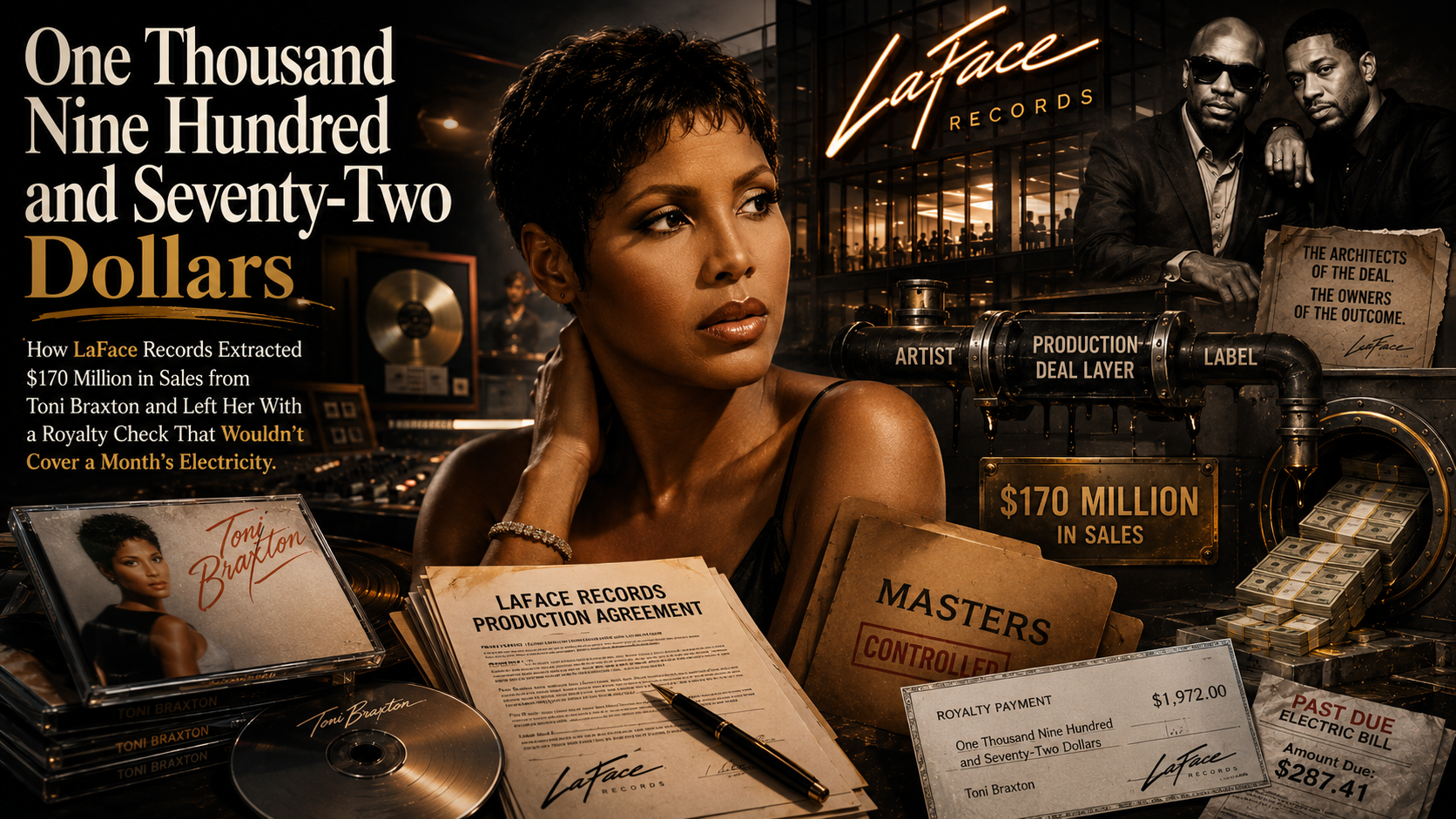

One Thousand Nine Hundred and Seventy-Two Dollars

How LaFace Records Extracted $170 Million in Sales from Toni Braxton and Left Her With a Royalty Check That Wouldn't Cover a Month's Electricity.

[THE LEDGER | AUDIT]

Investigative Standard & Intent This document is a product of The Multiverse and is grounded in Structural Imagination. The following analysis is a forensic examination of systems and architectures; it is not intended to target or attack any specific individual, institution, or company.

Every claim, figure, and contract term presented is drawn exclusively from verified public records and is fully attributed in the Reference Documents archive. This work is for the purposes of education, analysis, and civilisational record.

I. The Pattern LaFace Had Already Perfected

By the time Toni Braxton walked into the LaFace Records studio to record her self-titled debut album in 1993, the label and its parent Arista Records had already assembled the exact contract architecture that would be deployed against her. The recoupment provisions, the deduction of promotional expenses from royalties, the refusal to renegotiate even as commercial success mounted beyond any reasonable projection, the management of artist earnings through a chain of intermediaries, all of it had been tested and refined on TLC and would later be tested and refined again on Usher and others across the LaFace roster. Braxton arrived later than TLC but the mechanism waiting for her was already running.

Her debut album was released on July 13, 1993, and climbed to the top spot on the Billboard 200. Within its first four months it had sold 1.7 million copies. Within the full arc of its commercial life it generated an estimated $170 million in total sales revenue. At the contractual royalty rate of thirty-three cents per album sold, before the label applied its promotional expense deductions, Braxton's share of that revenue was already marginal. After those deductions, it became almost invisible. The royalty check she received from LaFace and Arista for the entire commercial run of her debut album was $1,972.

One thousand nine hundred and seventy-two dollars. Not per month. Not per quarter. In total. From an album that had generated one hundred and seventy million dollars in sales revenue. The ratio of what the institutional machinery surrounding Toni Braxton extracted to what it returned to her is not the result of market forces or complex economic calculation. It is the result of a contract structured to ensure that the person creating the value would receive the minimum the law permitted, and that the minimum the law permitted was, in practice, almost nothing.

The Silence That Was Enforced After TLC Spoke

In a later interview with Black Enterprise, Braxton disclosed something that illuminates the institutional response to TLC's Grammy stage declaration with particular clarity. She said that after TLC talked publicly about their bankruptcy, the label prohibited other LaFace artists from discussing their own financial situations. TLC had broken a carefully maintained silence, and the industry's institutional response was not to address the conditions that had produced that bankruptcy but to rebuild the silence as a contractual requirement imposed on the artists who remained.

Braxton herself was under this prohibition for years. When she eventually spoke, she was able to confirm that the pattern TLC had described was not unique to their situation. She had sold more than forty million records and received royalties of less than two thousand dollars. She also disclosed something that speaks to the legal architecture underpinning the entire structure: the issue had gone all the way to Congress around the question of whether bankruptcy law should protect recording artists the same way it protected every other category of commercial debtor. The answer from the legislative process, reflecting the lobbying power of an industry that had spent decades constructing these arrangements, was effectively no. Recording artists could file for bankruptcy but their recording contracts could not be discharged. They remained bound to the institutions that had produced their financial crisis even while formally insolvent.

II. The Two Bankruptcies and What They Actually Mean

The First Bankruptcy: 1998

In January 1998, Braxton filed for Chapter 7 bankruptcy. The filing revealed the full extent of the gap between what her commercial success had generated and what she had actually received. Her legal team confirmed during the proceedings that she was earning thirty-three cents per album sold and that the label had refused to raise that rate in two separate contract negotiations despite her being one of the most commercially successful artists on their roster. LaFace filed a countersuit citing breach of contract when she attempted to leave the deal. Under any equitable reading of the commercial relationship, an artist who had generated $170 million in sales and received a total royalty check of $1,972 has not received the agreed consideration for her work. The legal framework, however, was not designed around equity. It was designed around what had been signed.

Even Babyface, one of the co-founders of LaFace, acknowledged the problem when he was placed under oath and asked directly. A judge presiding over the case asked him not as a label executive but as an artist whether Braxton's deal was fair. His response, documented across multiple sources: if he had sold the records she had sold under those contract terms, no question, it was not fair. The person who helped build the institution that produced the unfair deal confirmed under oath that the deal was unfair. The institution's contractual and legal apparatus had nonetheless enforced it for years. The settlement that eventually emerged, reportedly worth $22 million to Braxton, represented not justice but a negotiated exit from a position the label recognised had become publicly untenable after the bankruptcy proceedings made the financial details visible.

Media coverage of the first bankruptcy repeated, with notable consistency, the characterisation that Braxton's financial difficulties were partly attributable to extravagant personal spending, specifically her purchase of dishes and home furnishings. Braxton addressed this directly, confirming that the items described in reports as extravagant were, in her own account, a $500 piece of flatware and TJ Maxx sheets at forty-nine dollars. She explained the mechanism that actually produced her financial crisis in one sentence: the label gives you an advancement on the next record and then the next record, so you kind of stay in debt, in a sense. The advance that sounds like income is a loan that extends the recoupment timeline. The artist is always in debt to the institution that is simultaneously selling their work to the public as a commercial product.

The Second Bankruptcy: 2010

The second bankruptcy, filed in 2010, involved debts ranging between ten and fifty million dollars and ultimately resulted in a total declared obligation of $18.3 million against assets of $1.6 million. The proximate cause was the collapse of her self-financed Las Vegas residency at the Flamingo Hotel, which was extended through 2010 after strong initial performance and then suddenly untenable when Braxton was hospitalised in 2007 with what was eventually diagnosed as lupus affecting her heart and other organs. She had personally financed the production costs of the residency show through her company Liberty Entertainment. When she could not perform, all of those costs became her personal debt with no revenue stream to service them.

The second bankruptcy is important to the structural analysis of this case not because it repeats the first but because of what it cost beyond money. As part of the resolution of her second bankruptcy filing, twenty-seven of the songs Toni Braxton owned the rights to, including You're Making Me High and Always, became available for bidding by creditors. They were purchased by a third party. An artist who had already received almost none of the commercial value her recordings generated for the institutions around her now lost ownership of the recordings themselves.

III. The LaFace Pattern: Why the Same Structure Produced the Same Results Twice

The fact that TLC and Toni Braxton experienced virtually identical financial outcomes from contracts with the same label at the same time is not a coincidence that requires elaborate explanation. It is the predicted output of a contract structure that was designed to produce it. The LaFace contract architecture, as revealed through the bankruptcy proceedings and litigation of both TLC and Braxton, included the same fundamental elements: a low base royalty rate, a comprehensive recoupment provision that included promotional expenses and advances, a refusal to renegotiate upward as commercial success escalated, and a contractual prohibition on discussing the financial details publicly.

What makes Braxton's case particularly significant as a companion to TLC's is that it demonstrates the structure's resilience even in the face of the public disclosure TLC had already forced. TLC spoke in 1996. Braxton filed in 1998. In the two years between those events, the label knew that its contract structure had produced a situation that three of its artists had been willing to declare publicly at the Grammy Awards. Its institutional response was not to change the structure but to prohibit other artists from doing the same. The silence was rebuilt. The structure continued and Toni Braxton paid the same price TLC had paid, to the same institution, for the same reasons.

"I sold more than 40 million records, yet my royalties were less than $2,000 dollars. All contracts are null and void except for a recording artist. Can you believe it?" - Toni Braxton, Black Enterprise

IV. The Royalty Rate as Policy, Not Error

It is important to be precise about what thirty-three cents per album sold means as a policy rather than an error. Thirty-three cents per album, before deductions, represents approximately three to four percent of the standard retail price of an album in the mid-1990s. The label was retaining ninety-six to ninety-seven percent of each album's retail value before applying any further deductions. After the deduction of promotional expenses, recording costs, and advances against the royalty account, Braxton's effective share of total revenue was a fraction of that already marginal rate. The $1,972 total royalty from $170 million in sales represents approximately 0.001 percent of the commercial value she generated.

No one at LaFace or Arista believed this represented fair compensation. Babyface said so under oath. The contractual and legal machinery, however, did not require the parties to believe the arrangement was fair. It required only that the arrangement was legal and had been signed. This is the definitional function of an exploitative contract structure: it separates what is fair from what is enforceable, and enforces what is not fair because it was agreed to at a moment when the power between the parties was so asymmetrical that the weaker party had no meaningful alternative to agreement.

Continued in Part 03: Usher - The Child in the Room When LaFace Set the Table.

EDITORIAL STATEMENT & LEGAL DISCLAIMER

Standard of Evidence

This document is produced by The Multiverse as an analytical and educational component of The Ledger: Sound and Fury. All arguments, models, and case studies are grounded in documented evidence, including public records, legal scholarship, sworn testimonies, and global financial disclosures. All data is cross-referenced with the Series Research Reference Document held in our archives.

Legal Notice & Intent

- Structural Imagination: The purpose of this work is education, analysis, and Structural Imagination. It is not designed to attack any specific name, institution, or company.

- No False Claim of Implementation: No claim is made that any specific individual or organisation will implement the solutions or frameworks proposed.

- Non-Advisory: This work does not constitute legal or financial advice.

- Methodology: Illustrative examples are clearly labeled, and every solution proposed is grounded in historical or legal precedent.

- Liability: The Multiverse assumes no liability for actions taken based on this analysis; the work of building a different creative economy begins with the knowledge that one is possible.